by Brian Shilhavy

Editor, Health Impact News

Donald Trump was swept into power in the November 2024 elections funded to a large extent by Silicon Valley billionaires.

In return for their support, Trump appointed JD Vance, who was handpicked by Silicon Valley as the Vice President. JD Vance is a disciple of Peter Thiel, who along with Elon Musk founded PayPal as part of the PayPal Mafia. See:

The Man Behind Trump’s VP Pick: It’s Worse Than You Think

Big Tech has been a huge part of Trump’s 2.0 Presidency, as we have seen here in 2025 with the push to make cryptocurrencies a larger part of the U.S. and worldwide financial system.

Before the end of the first quarter in March of 2025, the Trump family started their own cryptocurrency financial network to challenge traditional banking, called World Liberty Financial. I covered it back then. See:

Trump Takes on the Banking Industry by Developing his Own Cryptocurrency Financial Network

However, the most common way people use cryptocurrency today is through selling and buying it like an asset, which is why Blackrock and other giant Wall Street investors have created their own hedge funds around the price of cryptocurrencies.

To truly replace banks and become an entirely new financial system, crypto has to be used in financial transactions in places like the retail sector, where currently the credit card companies (Visa, Mastercard, etc.), backed by FDIC insured bank accounts, still dominate.

So in August this year, the Trump family-owned World Liberty Financial purchased a publicly traded Canadian company, Alt5 Sigma, giving World Liberty Financial a public stock listing in the U.S., and giving them an existing platform where cryptocurrencies were already being used for online payments in ecommerce stores and gaming sites.

Fast forward to today as we near the end of 2025, and things are not going well for Trump’s new crypto financial system, or its investors.

This was published this week on The Information:

Trump Family Crypto Deal Runs Aground

Crypto firm that did a complicated deal with the Trumps warns it may face lawsuits and regulatory probes.

By Michael Roddan

Excerpts:

Eric Trump and Donald Trump Jr. rang the bell at Nasdaq’s New York headquarters in August to celebrate the announcement of a deal that could have netted the family a windfall of hundreds of millions of dollars.

The president’s oldest sons were combining their crypto startup, World Liberty Financial, with a publicly traded Canadian company, Alt5 Sigma.

“We’re going to change finance forever,” Eric Trump said at the ceremony.

Alongside the Trump brothers were about two dozen people cheering the market open in front of a sign with the two companies’ logos.

Missing from the scene were any representatives of Alt5 Sigma, even the CEO. A World Liberty spokesperson said:

“other members of the Alt5 team were unable to attend.”

Troubles with the combined company quickly surfaced.

Weeks later, Alt5 suspended its CEO pending the outcome of an investigation by a new outside law firm, and the company warned staff it would likely face litigation and regulatory investigations, according to a letter from the firm distributed to employees.

Several other senior executives have quit or have been fired.

In the three months since, Alt5 Sigma’s shares have fallen 75% and the value of the Trumps’ crypto currency, $WLFI, has fallen by nearly half. The company also disclosed that it had been convicted of money laundering in Rwanda.

Alt5 told its staff on Sept. 4, without providing an explanation, about the suspension of its CEO. It didn’t publicly disclose the suspension until it posted a securities filing on Oct. 22.

Alt5 Sigma investors are furious.

“I feel betrayed,”

said Matt Chipman, a Los Angeles–based shareholder in the company. He said he had been stonewalled in his efforts to find out why the deal happened and what the company’s plans are.

The arrangement gave World Liberty Financial a public stock listing. The Trump family was aiming to profit from investor enthusiasm for digital asset treasury stocks—publicly traded companies whose sole purpose is to buy and hold crypto coins.

Founded by Canadian entrepreneurs in 2018, Alt5 Sigma built a trading platform and payment system that allowed customers to buy and sell crypto and to use digital coins to buy goods from e-commerce websites or gaming platforms.

It processed roughly $1 billion worth of transactions in 2023, according to company records and people familiar with the figures.

As part of the deal, World Liberty co-founder Zach Witkoff—the son of President Donald Trump’s Middle East envoy, Steve Witkoff—was appointed Alt5’s chair.

He said the deal would boost Alt5 Sigma’s original business by allowing it to issue cryptocurrencies that customers could use to make purchases.

But Alt5’s bet on the Trump cryptocurrency turned out to be awful.

The company’s stock is now more closely tied to the cryptocurrency than to its original business. Stocks that hold cryptocurrencies peaked in the summer and have tumbled since, with many falling by half or more.

Alt5 Sigma’s market capitalization has sunk from around $700 million before the deal to below $200 million.

Joining the Trump Orbit

Alt5 Sigma got its stock market listing last year through its merger with a biotech company, JanOne. The combined company named Canadian entrepreneur Peter Tassiopoulos as CEO.

Earlier this year, the Trumps’ World Liberty Financial was searching for a partner to help it issue crypto-enabled credit and debit cards.

Alt5 owned a subsidiary that could do just that. The two firms began discussing a possible project, former Alt5 employees said.

Those discussions didn’t pan out, but Tassiopoulos and the World Liberty team soon eyed a more adventurous opportunity: having Alt5 Sigma buy up the Trump’s cryptocurrency to join the burgeoning ranks of stocks that hold crypto. That led to the announcement at the Nasdaq.

World Liberty’s website says the Trump family owns 22.5 billion $WLFI tokens and is entitled to receive 75% of the proceeds from sales of the cryptocurrency. That implies the first part of the deal should have netted the Trumps roughly $550 million.

The second part, Alt5 Sigma’s purchase of tokens on the open market, could have boosted the value of $WLFI. The cryptocurrency was priced at 20 cents per token on completion of the deal.

Since then, however, the price has dropped as low as 11 cents, likely reducing the Trump family’s gains.

The American Consumer Still has More Power than they Realize

It is not surprising that the Trump family’s desire to create a financial system that would replace traditional banking with cryptocurrency has failed, forcing them to pivot to using cryptocurrencies as investment assets instead, just as the Wall Street hedge fund managers are doing.

To gain any traction in the payments sector and replace credit cards, consumers need to use it. And overwhelmingly in the U.S., consumers are NOT buying it, and prefer to stick with traditional banking and credit cards.

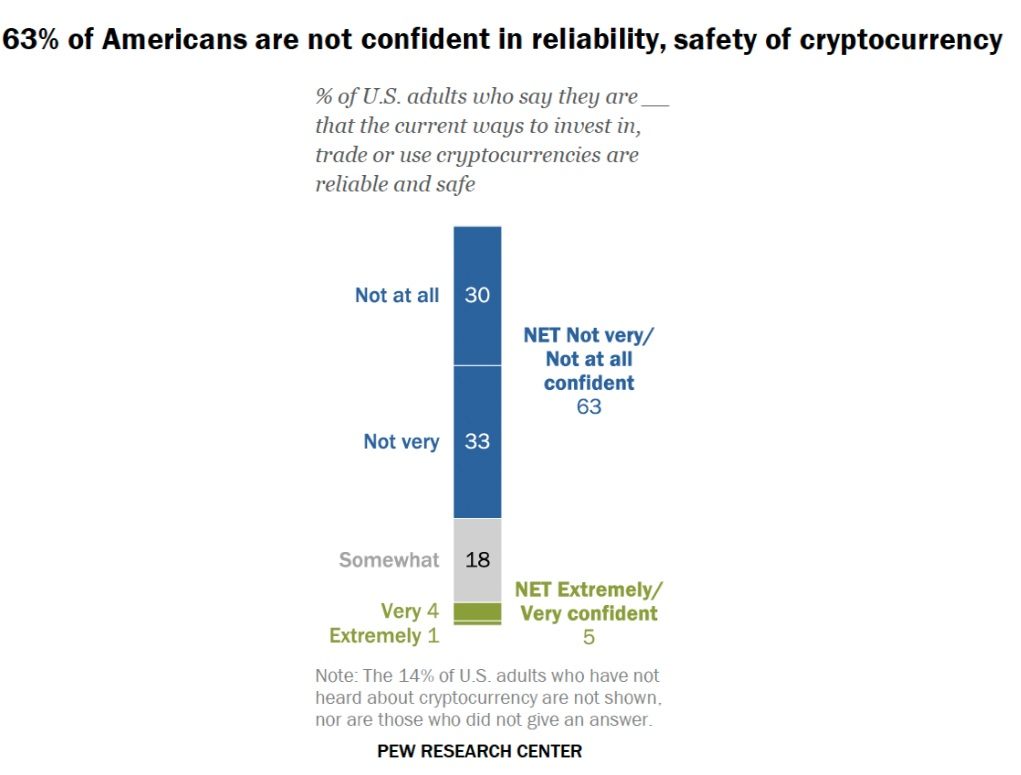

According to a Pew Research Center survey last year, in 2024, only 17% of U.S. adults say they have ever invested in, traded or used a cryptocurrency. They also report that this number remained roughly unchanged since 2021. (Source.)

Since these statistics are over a year old, I looked up data for this year, since Trump took over, since Trump has made the use of cryptocurrencies a major part of his administration.

It takes some digging to find, because almost everything written on cryptocurrencies is overly positive, comparing the use of cryptocurrencies to past years to project a huge growth in their adoption for the future, where Big Tech would love to have them replace banks so they can control the financial system.

So you have to read through the hype to get the actual numbers. For example, they will say that 85% of merchants around the world now accept some form of cryptocurrency for payments, without giving the actual number of customers who actually use crypto to buy things, compared to regular credit card transactions, even if a crypto payment was an option.

What I found is that most estimates for Americans using cryptocurrency in 2025 is still only around 20%, and the vast majority of those are using it as an investment asset, and are not using it for actual financial transactions in the real world.

Here is a good analysis from an industry publication on financial transactions:

Credit Cards vs. Crypto: What’s Winning in 2025

In the world of payments, two forces are shaping how we exchange money: credit cards and cryptocurrencies. Both methods have evolved since their inception.

Credit cards were introduced in the 1950s as a convenient way to make payments without cash. Cryptocurrencies, on the other hand, burst onto the scene in 2009 with the launch of Bitcoin and have seen explosive growth ever since.

As we move further into 2025, the debate continues: which form of payment is winning in terms of popularity, market share, security, and user trust?

In this article, we compare credit cards and cryptocurrencies from multiple angles, including user adoption, transaction volumes, security, and global market values in 2025.

Market Overview of Crypto and Credit Cards

The global payments industry has evolved at a fast pace and credit cards and cryptocurrencies are two of the major players vying for top positions. While credit cards have a long history and broad acceptance, cryptocurrencies have surged in popularity due to their innovative technology and potential for rapid growth.

Credit Card Market

- Global Credit Card Transactions: According to recent estimates, the total volume of credit card transactions worldwide is projected to reach USD 36 trillion in 2025. This is an increase from around USD 22 trillion in 2020 and reflects a growing trend toward cashless payments.

- Number of Credit Cards in Circulation: By the end of 2025, financial analysts expect there to be over 15 billion credit cards in circulation globally, up from around 11 billion in 2020. This includes both traditional credit cards and co-branded cards offered by airlines, retail stores, and technology companies.

- Card Penetration and Usage: Credit cards remain most popular in North America, Western Europe, and parts of Asia, where over 70% of adults have access to at least one credit card. In emerging markets, penetration rates are smaller but growing steadily.

Cryptocurrency Market

- Market Capitalization: The global cryptocurrency market capitalization is estimated to hover between USD 3 trillion and USD 5 trillion in 2025, depending on market conditions and regulatory developments. This is a significant rise from the roughly USD 250 billion to USD 1 trillion range seen in the late 2010s and early 2020s.

- Number of Cryptocurrencies: There are now over 10,000 cryptocurrencies, although only the top 20 hold a substantial share of the market. Bitcoin, Ethereum, Binance Coin, and several others remain the largest by market cap.

- Global Adoption Rate: As of 2025, around 8-10% of the global adult population owns some form of cryptocurrency, up from an estimated 1-2% in 2018. Cryptocurrencies have seen increasing acceptance by large retailers, payment providers, and cross-border remittance services. As of 2025, it’s estimated that over 85% of retailers worldwide accept credit cards in some form. Roughly 25% of online retailers accept crypto, but low single digits for physical stores.

User Adoption and Accessibility

When it comes to gaining a foothold in the global payments market, how easily and widely people can use a particular method is crucial. Credit cards have long been the gold standard, reaching billions of users through banks, retailers, and loyalty programs.

Cryptocurrencies, on the other hand, are redefining access in places where traditional banking might be limited, offering an alternative approach to cross-border transactions and financial services.

Credit Card Popularity

Credit cards remain a popular choice because they are widely accepted in brick-and-mortar stores, online shops, and for international payments. Other key factors include:

- Consumer Protection: Most credit cards come with fraud protection and the ability to dispute charges, building trust among users.

- Rewards and Incentives: Cash-back offers, travel miles, and loyalty programs encourage repeated card usage.

- Credit Building: Using a credit card responsibly can help individuals build a good credit score, leading to easier access to loans or mortgages.

Crypto’s Expanding Reach

Cryptocurrencies have gained traction as more people become comfortable with digital assets, especially in regions with less stable traditional banking systems. Key drivers of crypto adoption include:

- Lower Transaction Fees: International transfers in cryptocurrencies can be cheaper than wire transfers or credit card cross-border fees.

- Financial Inclusion: Cryptocurrencies offer an alternative financial system for the unbanked population, particularly in developing countries.

- Rapid Technological Innovation: The rise of DeFi, NFTs, and various blockchain-based solutions continues to draw in new users.

- Credit Cards: Trusted for decades, supported by banks, and widely accepted, credit cards benefit from a strong reputation and consumer protections. However, concerns over personal debt and hidden charges linger.

- Cryptocurrencies: While increasingly recognized, cryptocurrencies still face skepticism regarding price volatility and unclear regulation. Consumer trust has been growing steadily but remains below that of traditional banking systems.

Deciding who is “winning” between credit cards and crypto in 2025 depends largely on the criteria used:

- Total Transaction Volume: Credit cards are still ahead with over USD 36 trillion in global transactions. Crypto, while growing rapidly, handles much less in overall retail volume when compared to traditional finance (tradfi).

- Growth Rate: Cryptocurrencies outpace credit cards in terms of percentage growth, with transaction volumes rising over 25% annually. This suggests a significant shift in the payments ecosystem, although from a smaller base.

- Global Acceptance: Credit cards remain the most accepted payment method worldwide, but the acceptance of crypto has spread to more than 30% of large retailers in developed countries—an important milestone. The average merchant and small merchants rarely support credit cards yet.

- Security and Regulation: Credit cards enjoy mature security features and established regulations, whereas crypto benefits from blockchain’s inherent security but remains more vulnerable to hacking and scams. Both face ongoing regulatory challenges.

- Innovation: Crypto leads in innovation with decentralized finance, smart contracts, and rapid technological advancement. Credit cards maintain steady improvements in convenience and security.

In short, credit cards definitely remain the dominant force in everyday commerce due to their broad acceptance, consumer protections, and long-standing trust.

The Approaching Crypto Winter

Ken Brown, writing on finance and tech at The Information, published an article this week on the crypto market and the impending “Crypto Winter.”

Crypto Winter Will Be Different This Time

Excerpts:

Winter is coming, not just in the seasons but in the crypto market. If the current downturn turns into another crypto winter, it will have a bigger impact on the mainstream financial system than it has in the past.

Bitcoin has fallen 30% in less than two months and is down for the year, while other cryptocurrencies have crashed by much more.

This has occurred despite the most crypto-friendly regulatory environment ever.

What’s become clear is that instead of building an alternate financial system, the crypto industry used its newfound freedom to go crazy.

Some of this is just crypto being crypto. The thing to watch this year, and maybe the riskiest development in crypto, has been the rise of stablecoins.

These cryptocurrencies, which are pegged to the dollar, are the closest thing to an alternate financial system. The most boring part of crypto got blessed with a friendly new law dubbed the Genius Act, giving it instant credibility.

That’s led to a bunch of new stablecoin announcements and increased use, especially overseas. This week Klarna, the Swedish buy-now-pay-later provider, said it would launch a stablecoin called KlarnaUSD next year. They are joining payments company Western Union and cloud company Cloudflare in creating new offerings.

Stablecoins are currently dominated by Circle and Tether, which together have a market cap of roughly $250 billion.

Before we delve further into stablecoins, though, it’s worth looking more into the current meltdown.

Ground zero for the sell-off is a Singapore-based crypto exchange, Hyperliquid, that handles $13 billion in trades a day with 11 employees and offers staggering amounts of leverage. It was home to a $10 billion liquidation in October that ricocheted across markets. Hyperliquid also has a stablecoin.

On the traditional stock exchanges, crypto treasury stocks—listed companies stuffed with crypto—are among the biggest losers.

Until recently, the euphoria in crypto meant these stocks traded at a premium to their crypto holdings. Investors decided that paying $2 for every $1 of crypto was a good idea.

The companies logically issued stock or borrowed money to buy more crypto, driving up prices.

This trade has unwound painfully, and now the crypto treasury companies are trading at a discount to their holdings. The logical move for them is to sell crypto and buy back their shares. That cycle of selling can drive down prices.

All that is a reminder that stablecoins’ promise of zero volatility warrants some skepticism.

Because they are more closely linked to the financial system than any other form of crypto, stablecoins require more scrutiny and caution.

They are also closer to real money than anything else in crypto because they meet one crucial criteria of money–they are a store of value. Dogecoin can’t say that.

Stablecoins keep their 1:1 peg against the dollar by holding safe assets such as short-term Treasurys, bank deposits and money market funds. That’s legit, and is required by the stablecoin law.

It is ironic that stablecoins rely on traditional financial tools, which much of crypto disdains, to maintain their stability.

History has shown it’s easier to promise stability than to deliver it. Just this month, a small, fringe stablecoin blew up, wiping out around $200 million. The stablecoin, run by a company called Stream Finance, promised a yield of around 18% but collapsed after losing $93 million.

Stream Finance realized quickly that the promise of stability has a dark side—the bank run. While the company’s stablecoin operates differently than the major ones, the investor reaction is the same. It’s one thing to lose money on a risky investment.

It’s another to lose your savings. That invites panic, frantic withdrawals and crashes, and these have happened in every asset that promises to give people their money back in full.

“There has been a run, there will be a run, money market funds, repos, you name it, there will be a run,” said Lee Reiners, a fellow at the Duke Financial Economics Center and a former Federal Reserve official.

But memories are short, especially in crypto.

When Silicon Valley Bank failed in 2023, one of the biggest casualties was Circle, the dominant stablecoin in the U.S.

When Circle announced it had $3.3 billion of assets in SVB, it suffered its own bank run, and its stablecoin fell to 88 cents on the dollar. It was saved when regulators said the federal government would make all deposits at SVB whole.

As I said, memories are short. A crack in a money market fund led to one of the darkest moments of the 2008 global financial crisis. Drama in the Treasury market has caused several crises.

Stablecoins add another source of unpredictable risk to the financial system.

In retrospect, everyone will say we should have seen it coming.

The Information added a new reason to fear owning crypto: Home Robberies.

Crypto Robbery Rattles Investors

The recent bitcoin sell-off wasn’t the only cause for alarm among crypto investors this week. Many were rattled by news that a tech investor was robbed of $11 million worth of crypto at his home.

Doorbell camera footage shows someone posing as a delivery worker approaching the home, accessible on street level in Mission Dolores, and asking for “Joshua,” who opened the door. They then asked to borrow a pen and followed the victim into the home.

The investor—whom we’re not naming, to protect his privacy—was bound with duct tape and forced at gunpoint to give up his cellphone and laptop, containing the digital keys to his crypto accounts, the SF Standard reported.

The episode highlights a major vulnerability of crypto accounts compared with bank accounts.

A robber trying to shift large amounts of money out of a bank account will typically encounter questioning by the bank and often a delay of a few days—whereas crypto can be moved instantaneously.

That’s of course one of the advantages of crypto over traditional bank accounts, proponents have long argued.

But as the Saturday robbery demonstrates, it can work against crypto investors.

The Big Tech Collapse is Coming – Be Prepared

Almost everyone on Wall Street is now debating the collapse of the AI Bubble, whether we are near to it, or that it is still a long ways off, with very few now not acknowledging that a huge correction in the economy is coming due to our over-spending on Tech, and especially AI.

Google just introduced their latest version of Gemini, its new AI chat bot, which many are claiming is now the best AI chat bot available, eclipsing others like OpenAI’s ChatGPT.

This resulted in a huge increase in Google’s (ALPHABET) stock this week.

Google is apparently spending big to advertise its new AI, and I recently saw one of their new commercials advertising Gemini.

Was it promoting robots replacing humans and doing extraordinary things that everyone will want to buy? Did it promote how rich everyone is going to be because of this technology, like Elon Musk’s new religious dogma “Sustainable Abundance“?

Watch for yourself all the amazing things AI is going to do to radically transform our lives:

Wow, who wouldn’t want to invest in this amazing new AI technology! It will help you lie to your children better.

JUST SAY NO TO BIG TECH!

If you don’t use or purchase their products, they are powerless to make money off them. It really is that simple.

Now listen, you rich people, weep and wail because of the misery that is coming upon you. Your wealth has rotted, and moths have eaten your clothes. Your gold and silver are corroded.

Their corrosion will testify against you and eat your flesh like fire. You have hoarded wealth in the last days. (James 5:1-3)

Comment on this article at HealthImpactNews.com.

This article was written by Human Superior Intelligence (HSI)

See Also:

Understand the Times We are Currently Living Through

New FREE eBook! Restoring the Foundation of New Testament Faith in Jesus Christ – by Brian Shilhavy

What Kind of Person did Jesus Say was True with no Injustice in Them?

KABBALAH: The Anti-Christ Religion of Satan that Controls the World Today

Christian Teaching on Sex and Marriage vs. The Actual Biblical Teaching

Exposing the Christian Zionism Cult

The Bewitching of America with the Evil Eye and the Mark of the Beast

Jesus Christ’s Opposition to the Jewish State: Lessons for Today

Identifying the Luciferian Globalists Implementing the New World Order – Who are the “Jews”?

The Brain Myth: Your Intellect and Thoughts Originate in Your Heart, Not Your Brain

What is the Condition of Your Heart? The Superiority of the Human Heart over the Human Brain

The Seal and Mark of God is Far More Important than the “Mark of the Beast” – Are You Prepared for What’s Coming?

The Satanic Roots to Modern Medicine – The Image of the Beast?

Medicine: Idolatry in the Twenty First Century – 10-Year-Old Article More Relevant Today than the Day it was Written

Having problems receiving our emails? See:

How to Beat Internet Censorship and Create Your Own Newsfeed

We Are Now on Telegram. Video channels at Bitchute, and Odysee.

If our website is seized and shut down, find us on Telegram, as well as Bitchute and Odysee for further instructions about where to find us.

If you use the TOR Onion browser, here are the links and corresponding URLs to use in the TOR browser to find us on the Dark Web: Health Impact News, Vaccine Impact, Medical Kidnap, Created4Health, CoconutOil.com.